I. Executive Summary

This article gives a concise view of the global fatty acids sector (also called carboxylic acids or alkanoic acids), clarifying scope, size, and why it matters to buyers, producers, and investors.

Common Aliases

- Fatty acids; carboxylic acids; alkanoic acids

- Long-chain monocarboxylic acids; oleochemicals (as a product family)

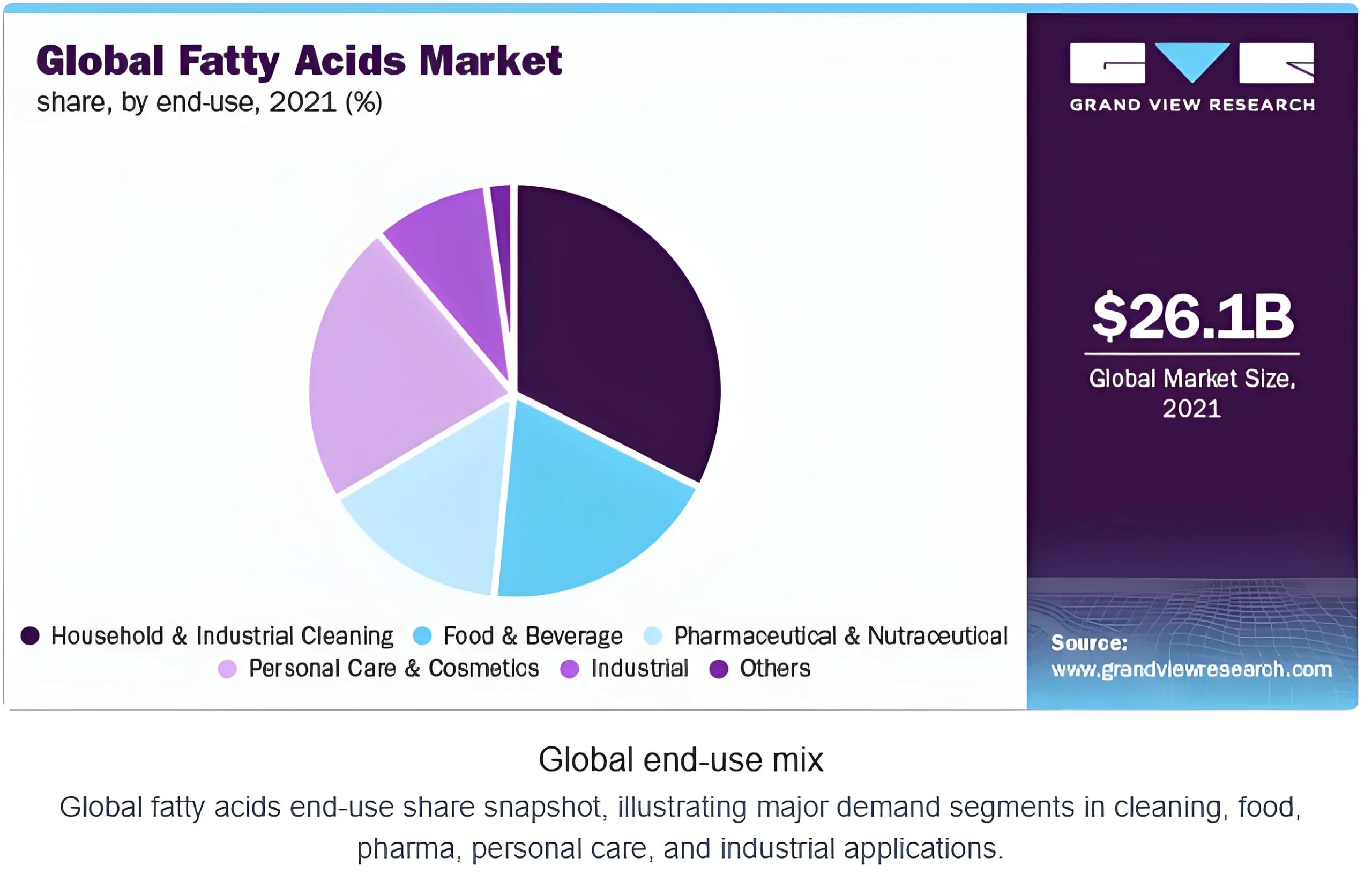

Core End-Use Sectors

- Food and nutrition (emulsifiers, acidulants), pharmaceuticals and nutraceuticals

- Soaps and detergents, personal care and cosmetics, industrial lubricants and surfactants

- Resin modifiers, rubber, paints and coatings, and specialty chemicals

Market Size and Growth

Published estimates vary widely due to scope differences (coverage of derivatives, chain-length ranges, and inclusion of soap noodles or specialty esters). Recent sources place 2024–2025 market value in a band from roughly USD 22–33 billion, while some broad-scope reports cite over USD 100 billion when downstream derivatives are included. Typical reported CAGRs for 2025–2032 cluster around 4–6%.

Why It Matters

Fatty acids are foundational to consumer staples (cleaning, personal care, food), to bio-based chemicals substitution, and to low-carbon supply chains. The industry’s shift to sustainable sourcing and energy-efficient separation is reshaping cost curves and risk profiles for global brands.

Regional Landscape (Indicative)

| Region | Role in Market |

|---|---|

| Asia-Pacific | Largest producer and consumer |

| Europe | Specialty grades, regulatory leadership |

| North America | Mature demand, innovation clusters |

| Latin America | Growing oleochemicals footprint |

| Middle East & Africa | Emerging consumption and logistics |

Global Fatty Acids Market Size Forecast

II. Supply Chain Analysis

This section maps the fatty acids industry value chain end-to-end and pinpoints where value accrues and risks emerge.

1. Upstream: Feedstocks

- Vegetable oils: palm, palm kernel, coconut, soybean, rapeseed; tall oil from pulping; used cooking oil in circular programs.

- Animal fats: tallow, lard—used where specs allow.

- Petrochemical routes: short-chain carboxylic acids; less common for C12–C18 volumes.

- Pre-processing: degumming/neutralization, bleaching, winterization, deodorization; quality metrics include FFA, moisture, impurities, and color.

2. Midstream: Core Conversion and Separation

- Hydrolysis (fat splitting) to produce mixed fatty acids and glycerin.

- Hydrogenation for saturation control; isomerization where needed.

- Fractional distillation and, for sensitive fractions, short-path/molecular distillation to isolate pure cuts (e.g., lauric C12, myristic C14, palmitic C16, stearic C18, oleic C18:1).

- Intermediates: mixed fatty acids, distilled fatty acids, hydrogenated fatty acids, and downstream esters (e.g., isopropyl myristate).

3. Downstream: Applications and Channels

- Soaps and detergents, surfactants, personal care emollients and thickeners.

- Food emulsifiers (through esters), nutraceuticals, and pharma excipients.

- Lubricants, metalworking fluids, rubber activators, plasticizers, coatings.

- Emerging uses: bioplastics, bio-lubricants, green solvents, agrochemicals.

Supply Chain Challenges and Practitioner Notes

- Feedstock volatility: Palm and lauric oils are exposed to weather, policy, and biodiesel mandates; integrated producers actively hedge and diversify feedstock baskets, and dual-qualify recipes to maintain continuity.

- Logistics: Liquid bulk coordination is critical—tank farm availability, ISO tank turnaround, and heating capabilities affect demurrage and product quality; during pandemic waves, we saw 2–4x lead-time spikes on certain lanes in Southeast Asia and EU.

- Sustainability: RSPO-certified palm streams (segregated or mass-balance) are increasingly required by top-tier FMCG customers; traceability programs combine supplier scorecards, satellite land-use checks, and mill audits to satisfy brand and regulatory expectations (e.g., EU deforestation regulation).

- Quality alignment: Food/pharma grades require tight peroxide, acid, and iodine values and robust change control; cross-contamination prevention and deodorization capacity are frequent bottlenecks when demand spikes.

III. Core Production Technologies (with Emphasis on Distillation)

This section explains the core production technologies, with a pragmatic focus on fractional distillation as the industry backbone.

Overview of Production Routes

- Hydrolysis (fat splitting): Triglycerides react with water under high temperature and pressure to yield fatty acids and glycerin.

- Hydrogenation: Adjusts saturation to meet performance or stability requirements.

- Fractional distillation: Separates fatty acids by boiling point under deep vacuum.

- Enzymatic methods: Low-temperature splitting using lipases for selective transformations; still niche but growing.

Fractional Distillation: Principle and Flow

- Process flow: Feed preheating → dehydration → vacuum column(s) with structured packing → side-draws by carbon number → polishing (short-path or reboiler trim) → deodorization/stripping → finishing tank.

- Operating conditions: Deep vacuum (often below 5–10 mbar) lowers boiling points to protect color and limit cracking; columns frequently exceed 20–30 meters with high-efficiency packing.

- Purity and specs: Commercial plants routinely deliver >95–98% single-cut purity; high-oleic or high-stearic specs are achievable with second-pass polishing.

- Advantages: High scalability, reliable cut consistency, broad feedstock tolerance, and proven quality control anchoring global standards.

- Limitations: Energy intensity, high capex for tall columns, materials selection (316L/duplex) to manage corrosion for tall-oil and certain byproducts, and skilled operations for vacuum integrity.

- Recent advances: Heat integration (multi-effect columns), mechanical vapor recompression on deodorization/stripping, advanced structured packing, model-predictive control for cut stability, and renewable steam or electrified reboilers to reduce Scope 1–2 emissions.

Practical Quality Control and Standardization

Routine analytics: GC-FID carbon-number profiling, acid value, iodine value, saponification value, color, peroxide value, odor threshold.

Standards and certifications: USP/NF and FCC for food/pharma, Kosher/Halal where applicable, ISO 9001/14001, and RSPO/ISCC for sustainable supply claims.

Comparison of Production Methods

| Method | Primary Purpose | Strengths | Constraints | Typical Use-Cases |

|---|---|---|---|---|

| Hydrolysis | Split triglycerides | Mature, scalable, co-produces glycerin | Requires energy and high-pressure kit | Base step for most oleochemical plants |

| Fractional Distill. | Purify by carbon number | High purity, flexible, industry standard | Energy and capex intensive | All major single-cut fatty acid production |

| Short-path Distill. | Gentle finishing/deodorization | Low thermal stress, protects color | Lower throughput | Premium grades, heat-sensitive fractions |

| Hydrogenation | Saturation adjustment | Stability, custom melting profile | Catalyst handling, selectivity control | Stearic-rich or oxidative-stable grades |

| Enzymatic Processes | Selective, low-temp conversions | Selectivity, potential lower footprint | Cost, enzyme lifetime, scale-up | Specialty esters, gentle splitting niches |

Production Technology Market Share

Fractional Distillation Process Parameters

IV. Industry Trends and Challenges

Key Trends

- Accelerating shift to bio-based and certified-sustainable fatty acids, driven by brand commitments and regulation; premium spreads for segregated palm streams are more accepted in tenders.

- Asia-Pacific deepens its lead via integrated complexes and proximity to lauric feedstocks; Europe grows in high-purity and pharma-grade niches; North America focuses on process intensification and nearshoring resilience.

- Technology progress in process intensification: better packing, advanced controls, heat pumps, and hybrid membrane–distillation pilots for specific cuts.

Challenges

- Raw material price volatility and policy shocks on edible oils; hedging and multi-feedstock qualification remain essential.

- Environmental regulation, from carbon pricing to deforestation-free rules, adds compliance cost but favors transparent suppliers.

- Supply chain disruptions from geopolitics and pandemics persist; tankage, vessel slots, and regional redundancy are key mitigations.

Brief Outlook

Expect steady mid-single-digit growth, with outsized gains in home and personal care, nutraceuticals, and bio-lubricants. The winners will combine assured sustainable feedstock access, energy-efficient distillation, and tight quality systems, while de-risking logistics and carbon exposure.

Global Fatty Acids Market Growth Forecast (2025-2032)

Segment Growth Index (2025=100)